Taking the right steps after an accident can mean the difference between getting your damages and costs covered through a car accident claim, or having to pay for everything out-of-pocket. Understanding the auto accident timeline and settlement process can help you manage expectations, reduce stress, and make informed decisions throughout the claims process.

1. Filing A Car Accident Claim

If you haven’t yet filed a claim with the negligent driver’s insurance company, your personal injury attorney will file a claim one for you. If you have, your attorney will notify the insurance provider that you are now represented on that claim.

Use our legal checklist to learn what to do after an accident and understand key legal considerations for recovering financial compensation.

2. Case Investigations

- After the car accident claim is filed, the insurance company investigates the accident to understand what happened, evaluate liability, and determine the total damages. The investigation is generally broken down into two parts–liability and damages.

Liability: This is the part of the investigation where the insurance claims adjuster determines fault for the accident. It can include:

- Photos

- Videos

- Witness statements

- The official police report following the car accident, if one exists.

Damages: This usually means either property damage or bodily injury/medical damages such as the following:

- Property damage – Once liability has been established, most property damage claims will resolve within a couple of weeks. In addition to covering the vehicle itself, it can also cover personal property, such as cell phones or car seats.

- Bodily injury/medical damages – Medical bills and lost wages incurred because of the accident are often a starting point. However, bodily injury claims can also include loss of companionship, pain and suffering, and other injuries that may not have a bill attached.

- Treatment – Even minor accidents can cause victims to need medical treatment for a couple of months. Serious injuries may need several months to a few years. The treatment and investigation phases of the settlement claim process often overlap in time.

3. Insurance Policy Review

State law typically determines who pays for medical bills, property damage, and other compensatory damages.

- In a comparative fault state such as Missouri (see Missouri’s at-fault auto policies), damages are allocated based on fault. For example, if one driver was 100% at fault, that driver’s insurance policy should (in theory) pay for 100% of the damages. On the other hand, if the driver was 90% at fault, the insurance provider will pay for 90% of the damages.

- In a modified comparative negligence state, such as Illinois, injured parties may recover damages only if they are less than 50% at fault for the accident.

- In “no-fault” states, such as Kansas, each driver’s own insurance initially pays property damage and medical bills regardless of how the accident happened. The insurance company for the at-fault driver only gets involved if the damages exceed certain thresholds.

Insurance companies and personal injury attorneys will carefully review both state law and the language of the policies involved. Insurance policy limits can strongly influence the payout in the car accident settlement process.

4. Settlement Demand

After treatment, investigation and policy review is complete, a personal injury attorney will send a demand, sometimes called a “demand letter,” to the insurance company. This legal document:

- Sets forth the plaintiff’s theory of the case.

- Lists the full extent of the plaintiff’s medical expenses and lost wages.

- Note any property damage, especially when the amount of property damage relates to the medical claims.

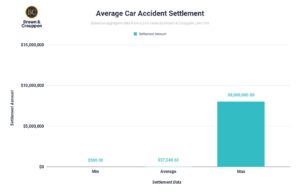

- Lists and explains any non-economic damages (such as pain and suffering). Generally, claims of pain and suffering have a higher payout – this can range from $1,000 to upwards of $100,000 depending on the injuries.

- Makes a demand for a desired settlement amount.

5. Settlement Negotiations

Once the demand letter is received by the insurance company, there are several possible responses.

- Demand letter is accepted and the case proceeds to finalize a settlement agreement.

- A counter offer is made and the negotiation process continues.

- The insurance company does not respond, requiring a follow-up.

- The claim is denied.

In this step, it’s important to work with an experienced personal injury law firm so that you understand potential outcomes and what is going to be in your best interest. Negotiations are one way car accident lawyers can help you obtain more money from your car accident settlement and maximize the value of your claim.

Were you injured in an accident due to someone else’s negligence? Get legal help from the most effective injury law firm in the Midwest.

6. Settlement VS Trial

Settlement

If settlement negotiations are finalized, the parties enter into a settlement agreement, which finalizes the compensation for the car accident claim and prevents any further legal action regarding the case.

Trial

If the parties cannot reach an agreement, a personal injury lawsuit may be filed in court to pursue compensation. Although most car accident cases are settled out of court, a trial may be needed if an insurance company does not respond, or refuses the payout of a fair settlement. An experienced car accident lawyer can help determine if a case should go to trial.

What to Do After a Car Accident (Legal Checklist)

If you’ve just been involved in a car accident, it’s important to follow these considerations…

1. STOP. Don’t just leave! Leaving the scene of an accident is a moving violation. It will result in points on your record, increased insurance premiums, and a ticket with a fine. And that is in addition to the property damage to your vehicle and any injury you might have received. (Moving your vehicle over to the side of the road is not “leaving the scene.”)

2) Call 911. Tell them that you have just been involved in an accident and give your location as best you can. Sometimes, law enforcement will not come to the scene, but will instead advise you to exchange information with the other driver. If this happens, you should still do a “walk in” at the police station to file an accident as soon as possible. Too often, insurance companies use the lack of a police report to either deny liability or downplay the severity of the accident.

3) Call your own car insurance company as soon as possible, even if you were not at fault. Most policies have language requiring you to inform them of an accident within a fairly short time frame, so be sure to let them know.

4) Gather as much information as you safely can, including:

- Insurance information of all parties involved.

- Name and phone number of people involved.

- Vehicle information (make, model, license plate) of those involved in the accident.

- Service/reference number of the police report and police officer information.

- Several pictures of your vehicle from different angles.

5) Don’t sign anything. If another driver’s insurance adjuster shows up at the scene, do not give a statement. Don’t answer any questions and don’t sign anything they give you.

6) If needed, get medical attention ASAP. Some injuries are immediately apparent after an accident, while others may take a few days to make themselves known. Seek medical attention as soon as you think you may be injured. A quick diagnosis can make things much better for you, both medically and legally, as the case goes on.

7) Call an experienced personal injury attorney. A lawyer can help you determine if you have a strong car accident claim, and help you pursue financial compensation for damages.

Most car accident settlements will follow the same steps in roughly the same legal process in the order below.

Get Help From a Car Accident Attorney at Brown & Crouppen Law Firm

In or out of court, it’s still highly beneficial to have the claim handled by a car accident attorney. An experienced attorney such as those at Brown & Crouppen Law Firm can help you receive a fair settlement offer, or file a lawsuit if insurance is unwilling to cooperate.

If you or a loved one has suffered injuries from a car accident, get help from a car accident attorney at Brown & Crouppen Law Firm. Getting started with your car accident case is easy. Call us at 888-802-8156 for a free consultation, or tell us about your case online with our free case evaluation form. And remember, there’s no upfront cost to you — if you don’t get paid, we don’t get paid.