Understanding The Financial Impact of Car Accidents—And How To Be Ready

A car accident can turn your life upside down in an instant. You’re suddenly dealing with emotional distress, possible physical injury, and expenses you didn’t plan for. From vehicle repair and medical costs to lost income and long-term increases in car insurance premiums, the unexpected costs of car accidents can strain your finances.

If you’ve recently been in a crash or know someone who has, you understand how overwhelming the experience can be. This guide will help you understand the financial impact of car accidents and offer actionable steps to protect your finances before the unexpected happens.

Navigating the Financial Aftermath of a Car Accident

The financial consequences of a car accident can begin accumulating as soon as metal hits metal. From the costs of injury treatment to motor vehicle repair or replacement, numerous unforeseen expenses can undo years of savings and significantly impact your financial well-being.

According to the National Highway Traffic Safety Administration, or NHTSA, motor vehicle crashes cost the U.S. $340 billion in 2019 alone. This staggering statistic is a reminder of how financially crippling a car accident can be, and how important it is to understand the potential costs.

Evaluating the Immediate Financial Costs

It’s easy to underestimate the costs you’ll incur after a collision. While total car accident expenses aren’t the same for everyone, understanding the main types of costs is crucial to protecting your finances.

Medical Costs

Safety is the priority after a crash. Before you do anything else, including trading insurance information, check for injuries and call emergency services.

It’s also essential to seek medical intervention for all injuries, including those that seem minor. Timely attention can prevent complications, identify hidden injuries, and help to document damage for insurance and legal purposes.

Medical costs may include:

- Emergency room visits and diagnostic procedures

- Ambulance charges for transportation to a medical facility

- Initial treatments, including surgeries, medications, or trauma care

- Short-term follow-up treatments, such as physical therapy or prescriptions

Initial car accident medical bills may be only the beginning for some accident victims, but even on their own, they can wreak havoc on your finances.

Insurance and Deductibles

While insurance is supposed to protect you from overwhelming costs, it rarely covers 100 percent of your out-of-pocket expenses. Most policyholders are responsible for paying a deductible before their coverage activates.

A deductible is the amount you agree to pay in case of a claim. If the repairs cost more than the deductible, your insurer will pay the remainder. You chose your deductible and selected your coverage when you signed up for your policy, unless you made changes more recently.

Understanding insurance coverage for car accidents is crucial to protecting your financial health. Relevant types of coverage include:

- Liability: Covers injuries and property damage your car causes

- Medical payments or personal injury coverage: Reimburses for your and your passengers' injury costs

- Collision: Covers damage from accidents and crashes with other objects

It’s essential to understand what your insurance covers and the limits of each coverage type. When you know your policy, you can navigate car crash costs and insurance with more clarity and control.

Vehicle Repair and Towing Costs

The cost of repairing or replacing your vehicle is one of the most immediate and visible financial consequences of an accident. Even minor collisions can cause significant body damage, mechanical problems, or safety issues that require professional repair.

Common necessary repairs include:

Windshield Replacement

$200 to $400

Scratch Repair

$150 to $2,500

Bumper Repair or Replacement

$100 to $2,000

Frame Damage Repair

$600 to $10k

Air Bag Replacement

$1k to $1.5k

Suspension Damage Repair

$1k to $5k

Engine Replacement

$1k to $7.5k

Lost Wages and Income Disruption

How Financial Stress Affects Your Mental Health

From medical bills to car repairs, the financial stresses of a car accident can be overwhelming. Anxiety, depression, and a feeling of losing control make it difficult to focus on recovery or make sound financial decisions.

Managing the stress of financial uncertainty is essential for your long-term well-being. To help you stay on track, here are some key financial tips for drivers after an accident:

Develop a Plan

Seek Knowledge Advice

Prioritize Mental Health

Reducing anxiety and depression helps you manage money better. Take time for yourself, do things you enjoy, and don’t be afraid to make an appointment with a therapist.

Financial stress can make it seem like nothing else matters, but your health comes first. If you’re less worried, you’ll make choices based on logic rather than panic.

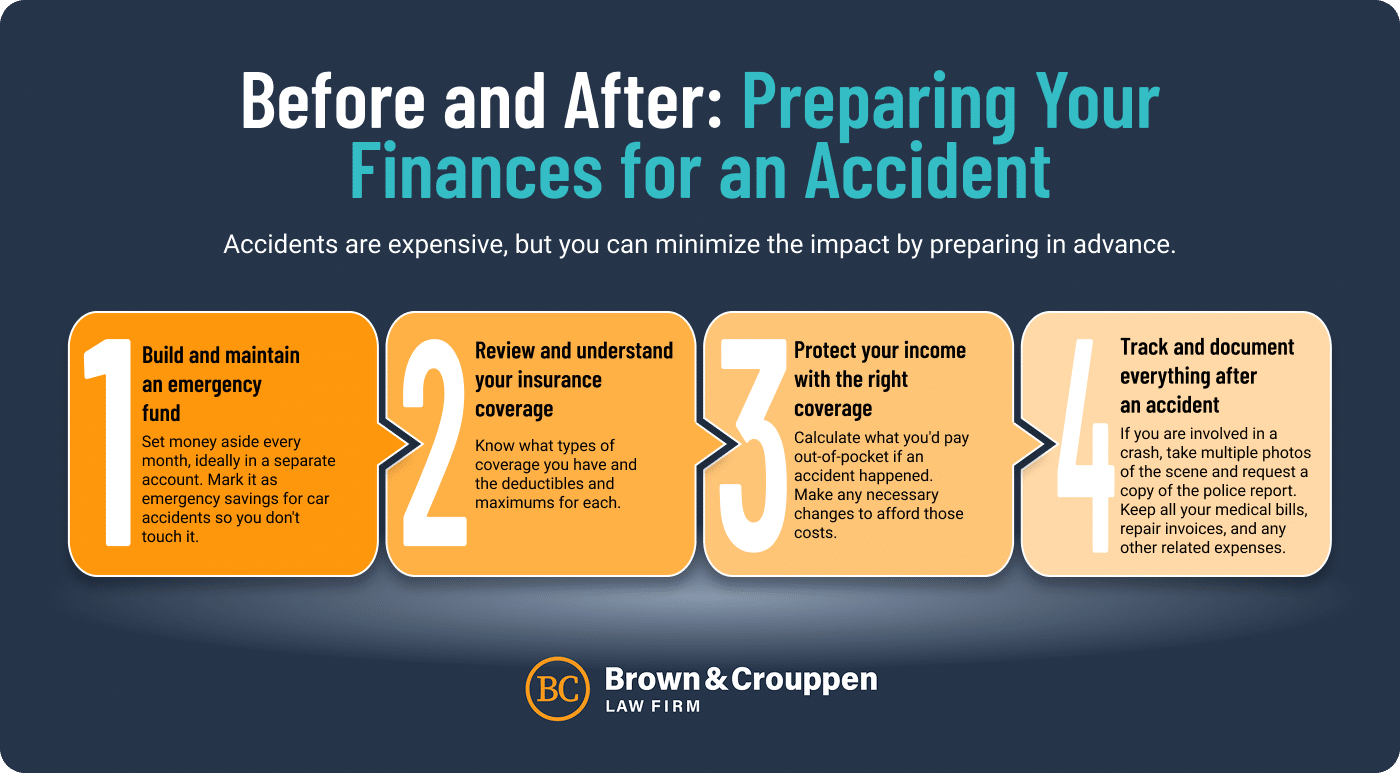

Actionable Advice and Financial Planning for Car Accidents

Financial preparedness for car accidents starts with proactive planning. Here are four key steps you can take to help protect your finances and minimize the fiscal impact of a crash.

Legal Implications and Costs After a Car Accident

Part of protecting your financial interests is understanding your legal rights and responsibilities after an accident. The more you know about the legal aspects, the more prepared you’ll be to pursue fair compensation for your damages.

Determining Liability and Legal Responsibilities

If you get into an accident, your ability to collect damages will depend at least partially on your degree of fault. States use fault determinations to determine whether you can file a lawsuit, how much you stand to collect, or both.

There are three basic systems:

Contributory negligence

Pure comparative negligence

Someone can collect compensation as long as they are less than fully at fault.

Modified comparative negligence

In both pure and modified comparative negligence states, the court reduces your award based on your percentage of fault. For example, someone 40 percent at fault would receive 60 percent of their compensation.

Filing Personal Injury Claims

Legal Fees and Associated Costs

When you’re already worried about your finances after an accident, hiring a lawyer can feel out of reach. Don’t feel intimidated. Many car accident lawyers, including Brown & Crouppen, work on a contingency fee basis.

When a lawyer works on contingency, you pay nothing unless you win. If you collect compensation, you pay an agreed-upon percentage of your award.

Legal Recovery and Financial Relief

Pursuing legal action is often the best way to get fair payment from an insurance company. Whether you settle out of court or go to trial, the compensation you receive can reduce stress and make recovery easier.

Long-Term Financial Effects After a Car Accident

When people consider the financial implications of car accidents, the first costs that come to mind are often medical bills, vehicle repairs, and lost wages. However, the long-term effects can be just as significant and even more detrimental.

Examples include:

- Insurance premium increases: Your premium is the annual cost of your car insurance. Accidents, especially at-fault accidents, often prompt the insurer to increase your premium. How much it increases and how long the higher rate lasts depend on your policy and where you live.

- Long-term medical costs: Serious injuries can necessitate prolonged medical treatment and ongoing supportive care, sometimes for years or a lifetime.

- Loss of earning potential: Lasting injuries or disabilities can impact your ability to work or advance in your career, costing you income.

- Impact on credit and debt management: Lasting injuries or disabilities can impact your ability to work or advance in your career, costing you income.

These consequences can last for months or years after the accident, impacting your overall financial stability and complicating your recovery.

Take Action Now To Protect Your Finances

The financial consequences of an accident can last long after you have recovered from your injury. By understanding these lasting effects and learning what to do financially after a car accident, you prepare yourself to weather the storm. From adjusting your budget and securing additional insurance to seeking legal and medical advice, the steps you take now can help you fare better later.

SCHEDULE A FREE CONSULTATION